Who we are

Magnetite Mines is an ASX-listed iron ore company focused on the development of magnetite iron ore resources in the highly-prospective Braemar iron region of South Australia. The Company has a total mineral resource of 6 billion tonnes of iron ore located 240km from Adelaide – 100% owned by Magnetite Mines.

Within these tenements, our flagship Razorback Iron Ore Project is the current focus. To give you a sense of perspective, our 2021 PFS for Razorback focused on just 8% of that resource, which is based entirely off our declared maiden Probable Ore Reserve of some 473 million tonnes.

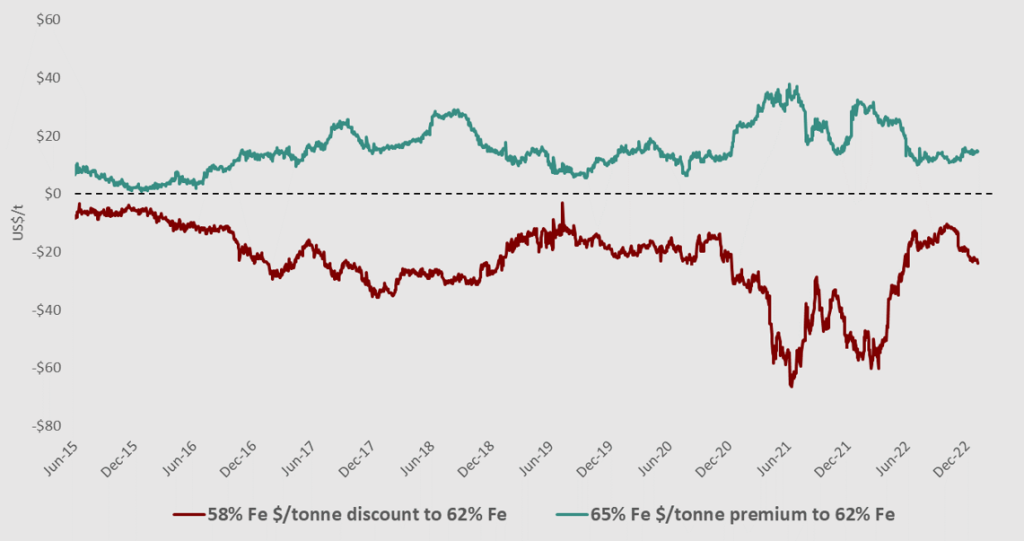

The Project will produce a premium high-grade iron ore concentrate at about 68% iron. We believe as general iron ore grades decline and steel mills face increasing pressure to decarbonise, the premium Razorback product will be in high demand.

Razorback has many unique geographical advantages. The iron ore is hosted in siltstone which is soft relative to WA magnetite ores and the resource outcrops, allowing for minimal stripping. The Project also benefits from access to existing infrastructure and is located close to heavy rail and existing iron ore ports.

High-voltage grid power is available, connecting to the main Southeast Australian grid, with a significant renewable energy component. While it would provide the Company with an estimated 70% renewable power supply today, the renewables intensity is forecast to be 100% when the mine commences production. The latest projections for the South Australia grid from the Australian Government Department of Industry, Science, Energy and Resources forecast 97% renewables by 2025.

ESG credentials are very important for resource projects, and we are well positioned to target a low-emissions footprint for our operations and products, with a higher-grade product helping steel mill customers in reducing emissions.

In July 2021, we completed our Pre-Feasibility Study (PFS) which optimised the project configuration around a 2.5Mtpa production capacity with a comparatively low and competitive capital cost. Following the positive results of the PFS, we moved directly to a Definitive Feasibility Study (DFS) for the Project in September 2021 and completed an Expansion Study in March 2022.

In response to rapidly-evolving market conditions and downstream industry feedback, the Company announced a strategic review in September 2022 to increase the planned production scale for the Razorback Iron Ore Project to a minimum of 5Mtpa and assess production options for high-value concentrate product streams. The expected benefits of this strategic shift include:

- enhanced project economics as a result of economies of scale and widening premiums for high-grade and DR-grade products, as demonstrated in recent Expansion Study outcomes.

- increased attractiveness to potential iron and steel industry partners and customers, institutional investors, and project financiers

- alignment of Project scale with large Mineral Resource Estimates

- potential to re-estimate Ore Reserves as a direct result of expanded production scale

- improved ESG credentials associated with enhanced concentrate specifications and potential electrification of key infrastructure and equipment supported by larger- scale development

Optimisation studies will be completed to determine a go-forward scope for a refocused DFS. These studies will include capacity options, expecting to result in an initial development scale at or above 5Mtpa, and scope options, including review of DR-grade concentrate production, transport and infrastructure options.

The optimisation studies will draw heavily on all work to date, including all transferable information from current DFS work streams. Accordingly, the optimisation studies are expected to be completed in a relatively short time frame with results expected in the first quarter of 2023. The timing for completion of the subsequent refocused DFS will be determined once the optimisation study results identify a go-forward scenario.

We have a very long-life iron ore project with expansion optionality in a tier 1 mining jurisdiction that will produce a superior iron ore product sought by steelmakers globally.

Premium Grade is a Major Advantage

PETER HANNAH FASTMARKETS/METAL BULLETIN

“To succeed in decarbonizing the global steelmaking industry there needs to be a greater recognition of how much the iron ore supply base needs to change. Vast volumes of existing production will need to be replaced by higher-grade supply, first to meaningfully reduce CO2 emissions from the prevailing BF/BOF technology, and later to meet the demands of a DRI sector at least an order of magnitude larger than it is today”

https://www.fastmarkets.com/article/3974510/iron-ores-critical-role-in-decarbonizing-steelmaking